(Original Video in Japanese was published on the FINOLAB CHANNEL on Oct. 15, 2024)

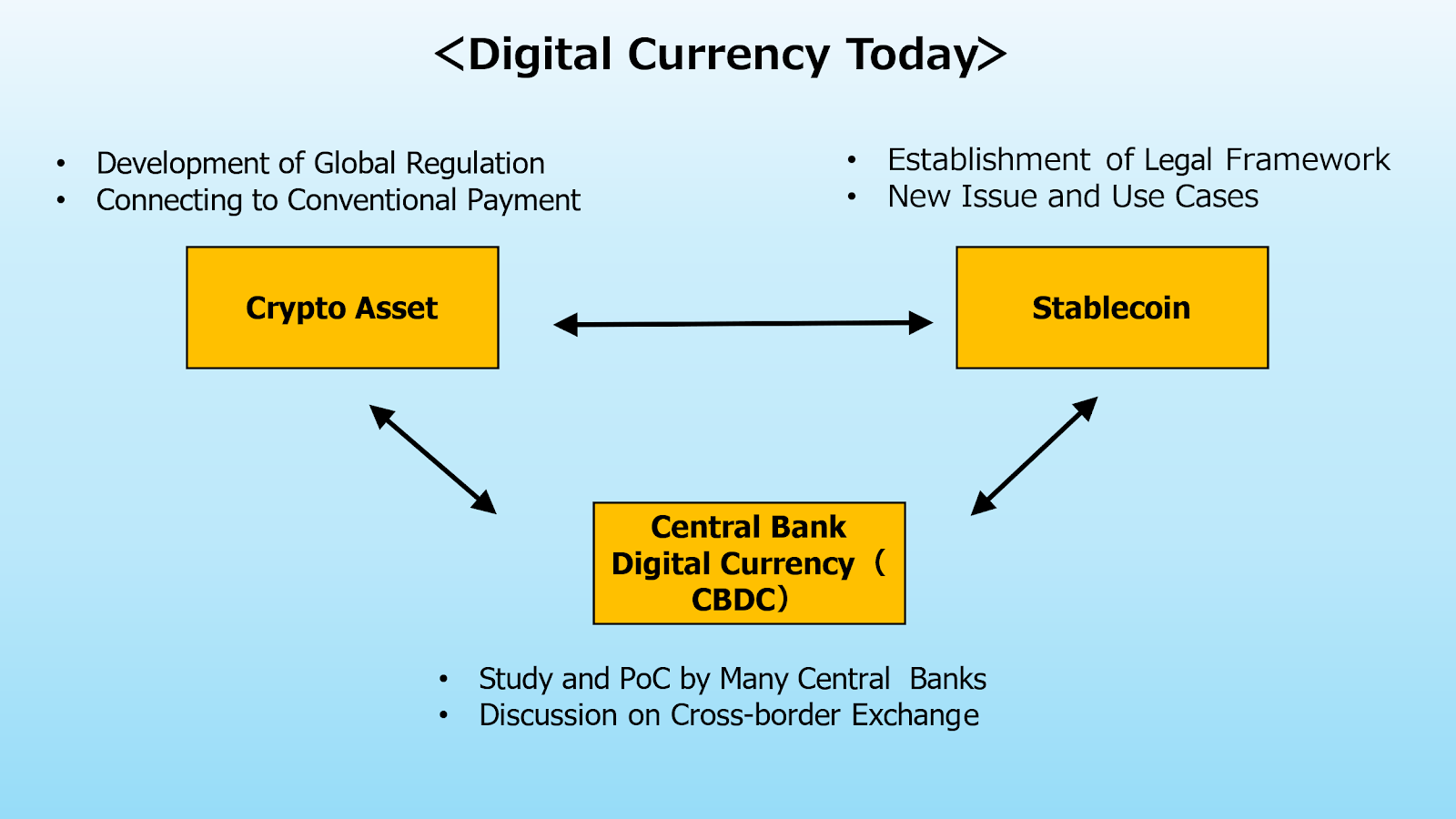

In recent years, discussions about digital currencies have intensified, particularly around the relationship between crypto assets, stablecoins, and central bank digital currencies (CBDCs). These forms of currency were once seen as independent competitors, but recent trends suggest they may have interdependent relations. We will share several related cases in this article.

<Central bank digital currency (CBDC)>

Central banks around the world have been actively researching and discussing CBDC. Although the daily use of CBDC may still take some time, the issue of cross-border CBDC exchange has become a main topic of discussion.

For example, the Monetary Authority of Singapore (MAS) has been exploring this through its Project Ubin+. Starting from their previous Project Ubin, which has gone through five phases of exploration since 2016, they have been conducting extensive research on CBDC. With the Ubin+ announced in November 2022, they are focusing on the study for cross-border CBDC transactions.

The Bank for International Settlements (BIS) and the Institute of International Finance (IIF) have jointly promoted an experiment called the “Agora Project,” which explores the feasibility of 40 major global banks and 7 central banks conducting cross-border settlements on a single platform. This experiment helps understand how CBDCs may be exchanged globally in the future and their potential collaboration with commercial banks.

<Stablecoin>

Globally, the legal framework for stablecoins is gradually being established, with countries formulating regulatory systems to ensure their widespread use in payment systems.

PayPal launched its stablecoin, PayPal USD (PYUSD), in August 2023, marking a significant move toward diversifying payment options. Although PayPal’s stablecoin has a relatively small market cap at the moment, its future potential cannot be overlooked. In the U.S. market, USDT (Tether) and USDC are the two largest stablecoins by market capitalization, both exceeding $10 billion in issuance. Meanwhile, PayPal’s PYUSD issuance is only $700 million. Nevertheless, with PayPal’s entry into the stablecoin market, the adoption of these currencies is expected to increase further.

In Europe, the stablecoin market is also gradually emerging. In June 2024, the Banking Circle launched the first euro stablecoin, EurL, in compliance with the EU’s Markets in Crypto-Assets (MiCA) regulatory framework. Although newly issued, the launch of this stablecoin marks an important step for Europe in stablecoin regulation and usage.

In Japan, the DCJPY network, created by Decurret DCP, has gained widespread attention. GMO Aozora Network Bank issued a yen stablecoin to settle environmental value in digital asset issued by IIJ on the network, providing new possibilities for digital currency use in Japan. This marks one of the significant milestones in Japan’s fintech sector.

<Crypto Asset>

Payment giant Stripe has begun exploring the potential of digital currency payments. Its crypto payment solution since Mar. 2022 with simple API allows merchants to accept cryptocurrency payments more easily.

Singapore-based startup dtcPay, which has partnered with VISA to create a payment system that allows both cryptocurrencies and stablecoins to be used as a funding source for transactions. The high-end card, VISA Infinite, is set to launch by the end of 2024. The target market for the card is affluent individuals who have accumulated wealth through investments in digital assets and high net worth individuals who added cryptocurrencies to their portfolio.

Triple A’s collaboration with Grab, a leading super-app in Southeast Asia, highlights another key development. In 2024, they announced the introduction of a feature that enables users to charge their Grab wallets with cryptocurrencies like Bitcoin and Ethereum, as well as stablecoins such as USDC, USDT, and XSGD. This marks a significant expansion in the functionality of Grab’s wallet, allowing users to seamlessly utilize digital currencies for a broader range of transactions.

<Conclusion>

These examples illustrate the rapid and dynamic changes in the world of digital currencies. Central bank digital currencies (CBDCs) are garnering increasing attention, particularly in discussions about international exchange mechanisms. At the same time, legal frameworks for stablecoins are being established in various countries, opening new pathways for their use in payments. Cryptocurrencies, once considered unsuitable for payments, are now becoming more integrated with traditional payment systems, as seen in the rise of crypto-linked cards, apps, and wallets.

The current trend indicates that digital assets are not just providing alternative payment but are beginning to coexist with traditional methods, creating new possibilities for the future of payments. As we would observe the actual deployment of CBDCs and the expanding use of stablecoins, the payment landscape is expected to undergo further transformation in the coming years.